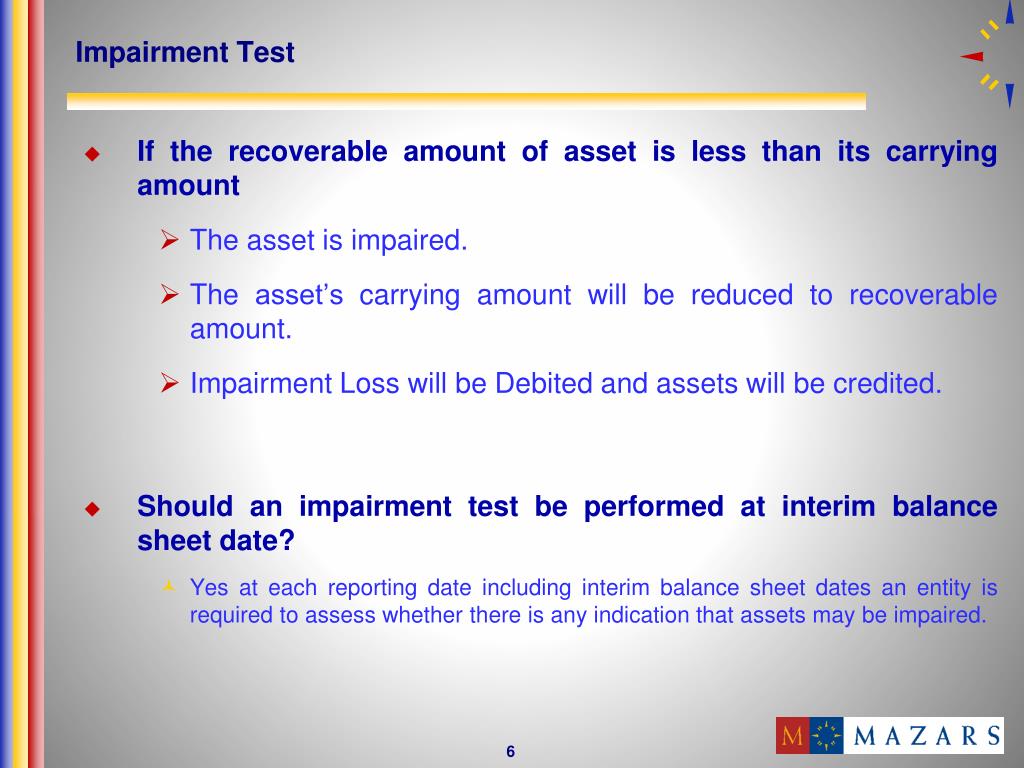

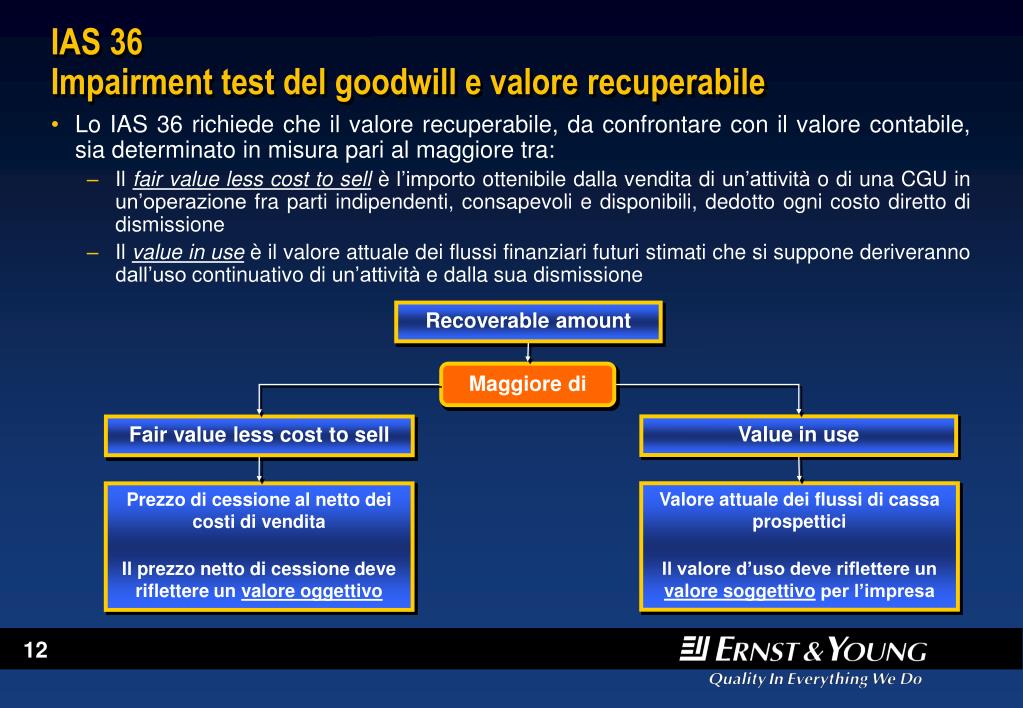

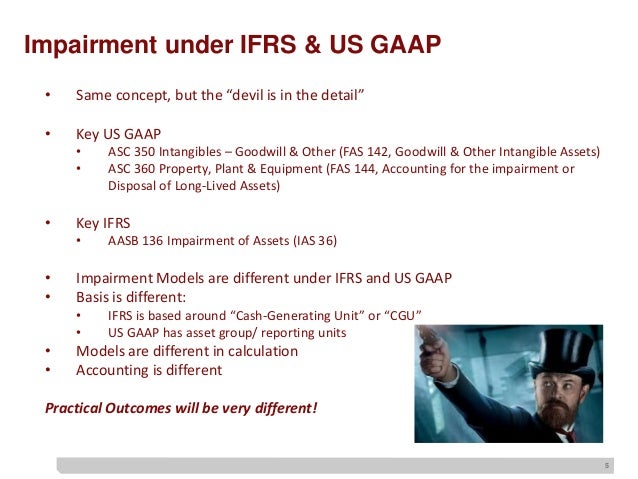

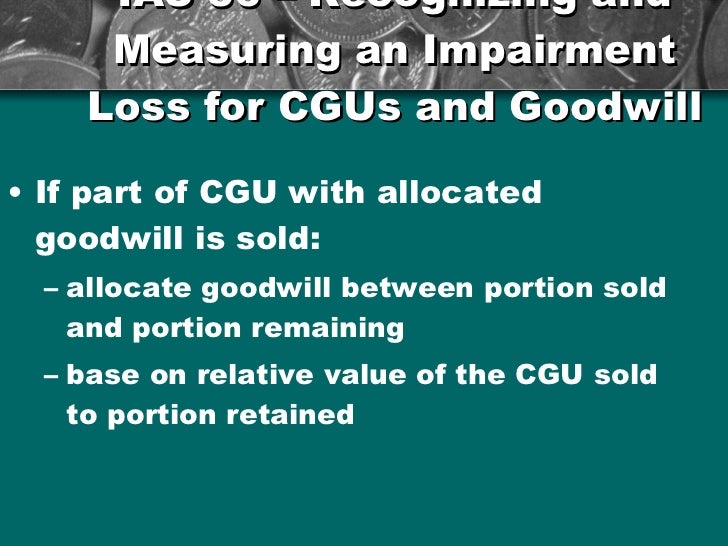

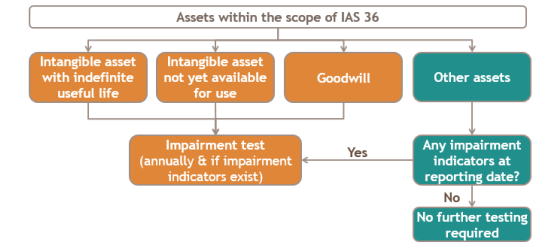

Ias 36 Impairment Test. For the requirements reference must be made to International Financial Reporting Standards. For impairment of an individual asset or portfolio of assets, the discount rate is the rate the entity would pay in a current market transaction to To test for impairment, goodwill must be allocated to each of the acquirer's cash-generating units, or groups of cash-generating units, that are expected.

The objective of this Standard is to prescribe the This impairment test may be performed at any time during an annual period, provided it is performed at the same time every year. __EC_TEST__. annualreturns.icaew.com.

Used to remember if the user is accessing the website on a computer or mobile device.

IAS 36 Impairment of Assets | Abdelhamid & Co Certified Public Accountants & Auditors

ACCA F7 by Elshan Rahimoff. IAS 36 "Impairment of Assets" - YouTube

Impairment-Test nach IAS 36 - Prof. Dr. Stefan Thiele - Bergische ...

Der Impairment Test nach IAS 36 | Hausarbeiten publizieren

IAS 36 Impairment of Assets – IFRSbox – Making IFRS Easy

UNIT 2 - Practice Questions (IAS 36 Impairment of Assets)[1] - UNIT 2 Practice Questions(IAS 36 ...

PPT - IAS 36 Impairment of Assets PowerPoint Presentation, free download - ID:498491

How to Make Cash Flow Projections for Impairment Testing under IAS 36 - IFRSbox - Making IFRS Easy

Werthaltigkeitsprüfung. Der Impairment Test nach IAS 36 | Hausarbeiten publizieren

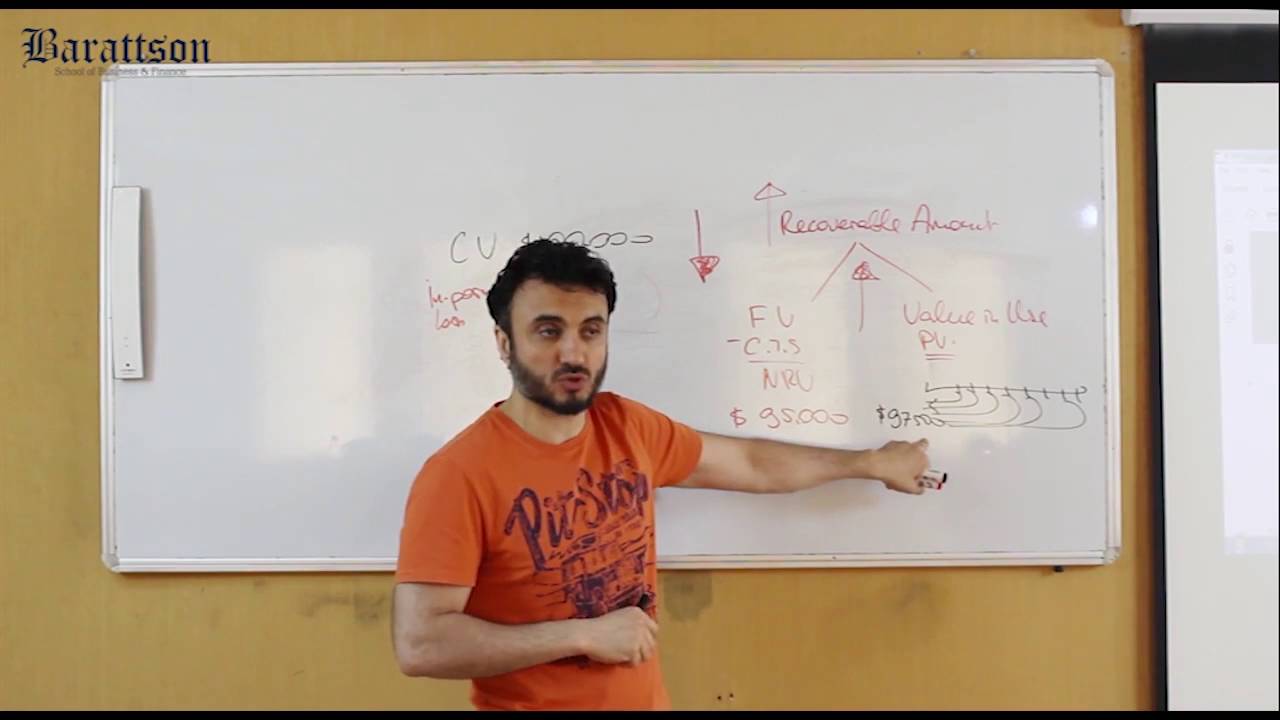

How to test impairment of fixed assets - IAS 36 - video tutorial on Vimeo

Werthaltigkeitsprufung. Der Impairment Test Nach IAS 36 - Walmart.com - Walmart.com

How to Make Cash Flow Projections for Impairment Testing under IAS 36 - IFRSbox - Making IFRS Easy

PPT - IFRS 3 – IAS 36 PowerPoint Presentation, free download - ID:3623941

Impairment Testing nach IFRS 3 und IAS 36 | Hausarbeiten publizieren

Der IFRS Goodwill Impairment Test | SpringerLink

Der Impairment Test gem IAS 36: Ermessensspielrume und bilanzpolitische Gestaltu 9783656336662 ...

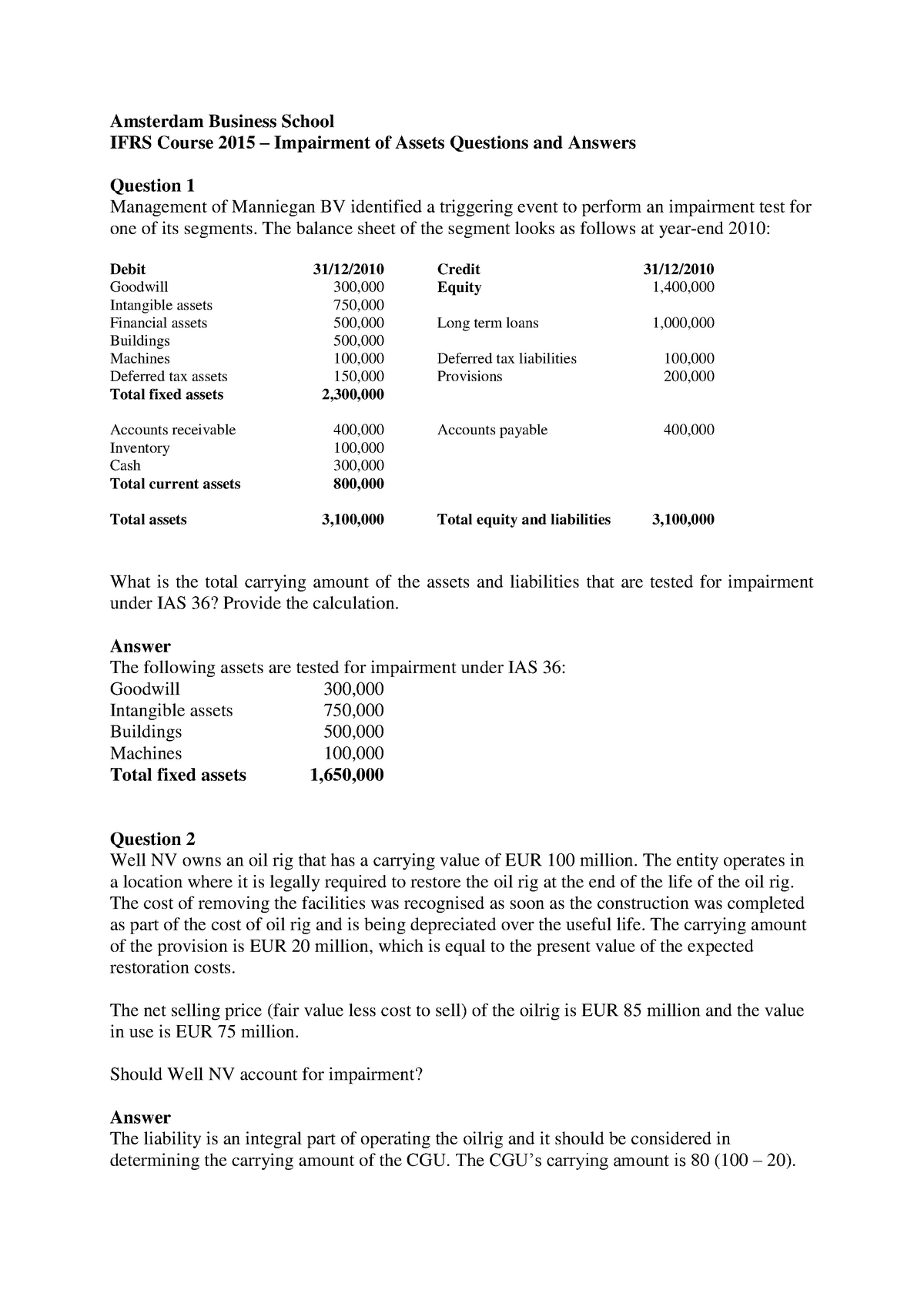

Week 2 Ias 36 - Questions and Answers - 6314M0030Y: International Financial Reporting Standards ...

Тест на обесценение активов МСБУ 36 (IAS) impairment test - Оценочная компания "Expert IN"

IAS 36 Impairment of Assets - IFRSbox - Making IFRS Easy

Impairment of Assets (IAS 36) - Part 1 - YouTube

PSAK-48- IAS 36: Impairment -ias-36

IFRS 16 e IAS 36: L'Impairment test dei diritti d'uso - Akeron Consulting

Ein gelungener Impairment-Test nach IAS 36 - Controller Institut Insights

Impairment of Assets according to IAS 36 - white paper

Impairment Presentation 2015

PPT - IAS 36 Impairment of Assets PowerPoint Presentation - ID:498491

Impairment Test of Goodwill under IAS 36 by claudio Passoni on Prezi

Folge 6.4: DPR-Prüfungsschwerpunkte 2020 – Impairment Test (IAS 36) - YouTube

Ias 36

Calculate Value in Use under IAS 36 - Magnimetrics - Medium

Kulturelle Einflüsse auf die Anwendung des Impairment-Tests nach IAS 36 - Voets Christina - Lang ...

Specific Provisions of IAS 36 – Impairment of assets and its implication on Financial Reporting ...

IFRS 16 e IAS 36: L'Impairment test dei diritti d'uso - Akeron Consulting

PPT - IAS 36 Impairment of Assets PowerPoint Presentation, free download - ID:498491

IAS 36 Impairment of Assets – IFRSbox – Making IFRS Easy

IAS 36IE Impairment Testing CGU With Goodwill And NCI – FAQ | IFRS

IFRS IN PRACTICE / IAS 36 Impairment of assets

Ein gelungener Impairment-Test nach IAS 36 - Controller Institut Insights

Redução ao valor recuperável de ativo - CPC 01 - Teste de Impairment - IAS 36 - Impairment test ...

IAS 36 - IMPAIRMENT OF ASSETS | ACCA SHARERS

IFRS is easy: 10 (Ten) Case Study Solutions on IAS 36 –Impairment of Assets

IAS 36, goodwill, intangibles, PPE impairment disclosures, VIU basis, sensitivity analysis ...

Teste de Impairment conforme o IAS 36. Figure 2 – Impairment testing... | Download Scientific ...

Impairment Test – ControllingWiki

L' Economostro: Impairment Test e IAS 36 per il Parlamento Italiano

PPT - IAS 36 Impairment of Assets PowerPoint Presentation, free download - ID:498491

Ias 36

(PDF) Goodwill Impairment Test Disclosures Under IAS 36: Disclosure Quality and its Determinants ...

IFRS 6 Impairment of Exploration Assets | Auditor Room

In asset impairment, how do companies settle on a fair value of the asset in question? - Quora

Michele Barsanti - Akeron Consulting

The US GAAP impairment guidance doesn't mentions recoverable amount. For the requirements reference must be made to International Financial Reporting Standards. For impairment of an individual asset or portfolio of assets, the discount rate is the rate the entity would pay in a current market transaction to To test for impairment, goodwill must be allocated to each of the acquirer's cash-generating units, or groups of cash-generating units, that are expected.